Simple and Compound Interest Calculator – Complete Guide to Interest Calculation

Have you ever taken a loan and wondered how the bank calculates the interest you pay? Or maybe you have money in a savings account and want to know how much it will grow over time?

I remember taking my first car loan. The dealer told me the interest rate was 5% and my monthly payment would be $377 for 5 years. I had no idea how they arrived at that number. I thought 5% of $20,000 is $1,000, so why was I paying so much more?

Later, I learned about simple and compound interest. I realized that car loans use simple interest, but credit cards use compound interest. Understanding the difference saved me thousands of dollars over the years.

This guide will teach you everything you need to know about interest calculation. What simple interest is, what compound interest is, how they differ, and how to calculate both.

Quick access: Use our free interest calculator here

What is Interest? Simple Answer

Interest is the money you pay for borrowing money (loan) or the money you earn for lending money (savings).

Simple example:

- You borrow $1,000 from a bank at 10% interest per year

- After 1 year, you owe the bank $1,000 + $100 interest = $1,100

- The $100 is the interest

Think of interest as a rental fee. You are renting money from the bank, and the interest is your rent payment.

Simple Interest vs Compound Interest – What is the Difference?

This is the most important thing to understand. The difference can cost or earn you thousands of dollars.

Simple Interest

Simple interest is calculated only on the original amount (principal). You never pay interest on interest.

Example: $10,000 at 10% simple interest for 5 years

| Year | Principal | Interest This Year | Total Interest | Total Owed |

|---|---|---|---|---|

| 1 | $10,000 | $1,000 | $1,000 | $11,000 |

| 2 | $10,000 | $1,000 | $2,000 | $12,000 |

| 3 | $10,000 | $1,000 | $3,000 | $13,000 |

| 4 | $10,000 | $1,000 | $4,000 | $14,000 |

| 5 | $10,000 | $1,000 | $5,000 | $15,000 |

Total interest paid: $5,000

Compound Interest

Compound interest is calculated on the original amount PLUS any accumulated interest. You pay interest on interest.

Example: $10,000 at 10% compound interest for 5 years

| Year | Starting Balance | Interest This Year | Ending Balance |

|---|---|---|---|

| 1 | $10,000 | $1,000 | $11,000 |

| 2 | $11,000 | $1,100 | $12,100 |

| 3 | $12,100 | $1,210 | $13,310 |

| 4 | $13,310 | $1,331 | $14,641 |

| 5 | $14,641 | $1,464 | $16,105 |

Total interest earned: $6,105

The difference: Compound interest gave you $1,105 more than simple interest over 5 years. Over 20 years, the difference is huge.

Simple Interest Formula – How to Calculate

Simple interest is straightforward. Here is the formula and how to use it.

The Simple Interest Formula:

SI = (P × R × T) ÷ 100

Where:

- SI = Simple Interest

- P = Principal (the amount you borrow or invest)

- R = Rate of interest per year (in percentage)

- T = Time in years

Then total amount = P + SI

Example 1: Car Loan

Scenario: You take a car loan of $20,000 at 6% simple interest for 5 years.

Step 1: SI = (20,000 × 6 × 5) ÷ 100 = (600,000) ÷ 100 = $6,000

Step 2: Total amount = $20,000 + $6,000 = $26,000

Step 3: Monthly payment = $26,000 ÷ 60 months = $433.33

What this means: You pay $6,000 in interest over 5 years. Each year, you pay $1,200 in interest.

Example 2: Short-Term Loan

Scenario: You borrow $5,000 at 12% simple interest for 2 years.

Step 1: SI = (5,000 × 12 × 2) ÷ 100 = (120,000) ÷ 100 = $1,200

Step 2: Total amount = $5,000 + $1,200 = $6,200

What this means: You pay $1,200 in interest over 2 years. Each year, you pay $600 in interest.

Example 3: Savings Account (Simple Interest)

Scenario: You deposit $10,000 in a savings account paying 3% simple interest for 3 years.

Step 1: SI = (10,000 × 3 × 3) ÷ 100 = (90,000) ÷ 100 = $900

Step 2: Total amount = $10,000 + $900 = $10,900

What this means: Your money grew by $900 over 3 years.

Compound Interest Formula – How to Calculate

Compound interest is slightly more complex, but the formula is easy once you understand it.

The Compound Interest Formula:

A = P × (1 + r ÷ n) ^ (n × t)

Where:

- A = Final amount (principal + interest)

- P = Principal (initial amount)

- r = Annual interest rate (as a decimal, so 10% = 0.10)

- n = Number of times interest compounds per year

- t = Time in years

Then Compound Interest = A - P

Compounding Frequencies Explained

| Frequency | n value | How often |

|---|---|---|

| Annually | 1 | Once per year |

| Semi-annually | 2 | Twice per year (every 6 months) |

| Quarterly | 4 | Four times per year (every 3 months) |

| Monthly | 12 | Every month |

| Daily | 365 | Every day |

Example 1: Annual Compounding

Scenario: You invest $10,000 at 8% compounded annually for 10 years.

Step 1: P = $10,000, r = 0.08, n = 1, t = 10

Step 2: A = 10,000 × (1 + 0.08 ÷ 1) ^ (1 × 10) Step 3: A = 10,000 × (1.08) ^ 10 Step 4: A = 10,000 × 2.1589 = $21,589

Step 5: Interest = $21,589 - $10,000 = $11,589

What this means: Your $10,000 more than doubled in 10 years without you adding any money.

Example 2: Monthly Compounding

Scenario: Same $10,000 at 8% but compounded monthly for 10 years.

Step 1: P = $10,000, r = 0.08, n = 12, t = 10

Step 2: A = 10,000 × (1 + 0.08 ÷ 12) ^ (12 × 10) Step 3: A = 10,000 × (1 + 0.006667) ^ 120 Step 4: A = 10,000 × (1.006667) ^ 120 Step 5: A = 10,000 × 2.2196 = $22,196

Step 6: Interest = $22,196 - $10,000 = $12,196

What this means: Monthly compounding gave you $607 more than annual compounding on the same $10,000 over 10 years.

Example 3: Daily Compounding

Scenario: $10,000 at 8% compounded daily for 10 years.

Step 1: A = 10,000 × (1 + 0.08 ÷ 365) ^ (365 × 10) Step 2: A = 10,000 × (1.000219) ^ 3650 = $22,253

Interest: $12,253

Comparison table:

| Frequency | Final Amount | Interest Earned | Extra vs Annual |

|---|---|---|---|

| Annually | $21,589 | $11,589 | Base |

| Quarterly | $22,080 | $12,080 | +$491 |

| Monthly | $22,196 | $12,196 | +$607 |

| Daily | $22,253 | $12,253 | +$664 |

When to Use Simple vs Compound Interest

Understanding when each type applies is crucial for financial planning.

When Simple Interest is Used

Car loans: Most auto loans use simple interest. The interest is calculated on the original principal.

Personal loans: Many personal loans use simple interest, especially fixed-rate loans.

Some student loans: Federal student loans often use simple interest.

Short-term loans: Loans under 1 year often use simple interest.

When Compound Interest is Used

Credit cards: Credit cards use compound interest (daily compounding). This is why credit card debt grows so fast.

Savings accounts: Most savings accounts use compound interest (daily or monthly).

Investment accounts: Stocks, mutual funds, and retirement accounts use compound interest.

Mortgages: Home loans use compound interest (usually monthly).

Fixed deposits / CDs: These use compound interest (varies by bank).

The Power of Compounding – Real Examples

Compound interest is called the "eighth wonder of the world" for a reason. Here is why.

Example: Two Friends, Different Start Times

Friend A: Starts investing $5,000 per year at age 25 Friend B: Starts investing $5,000 per year at age 35 Both earn 8% returns and invest until age 65.

Friend A (starts at 25):

- Invests for 40 years

- Total invested: $200,000

- Final amount at 65: $1,295,000

- Total profit: $1,095,000

Friend B (starts at 35):

- Invests for 30 years

- Total invested: $150,000

- Final amount at 65: $566,000

- Total profit: $416,000

The difference: Friend A invested only $50,000 more but ended with $729,000 more. The 10-year head start was worth $729,000.

Example: Small Monthly Investments

Scenario: You invest $200 per month from age 25 to 65 (40 years) at 8% returns.

- Total invested: $200 × 12 × 40 = $96,000

- Final amount: About $620,000

- Total profit: $524,000

What this means: For less than $100 per week, you can become a millionaire by retirement age.

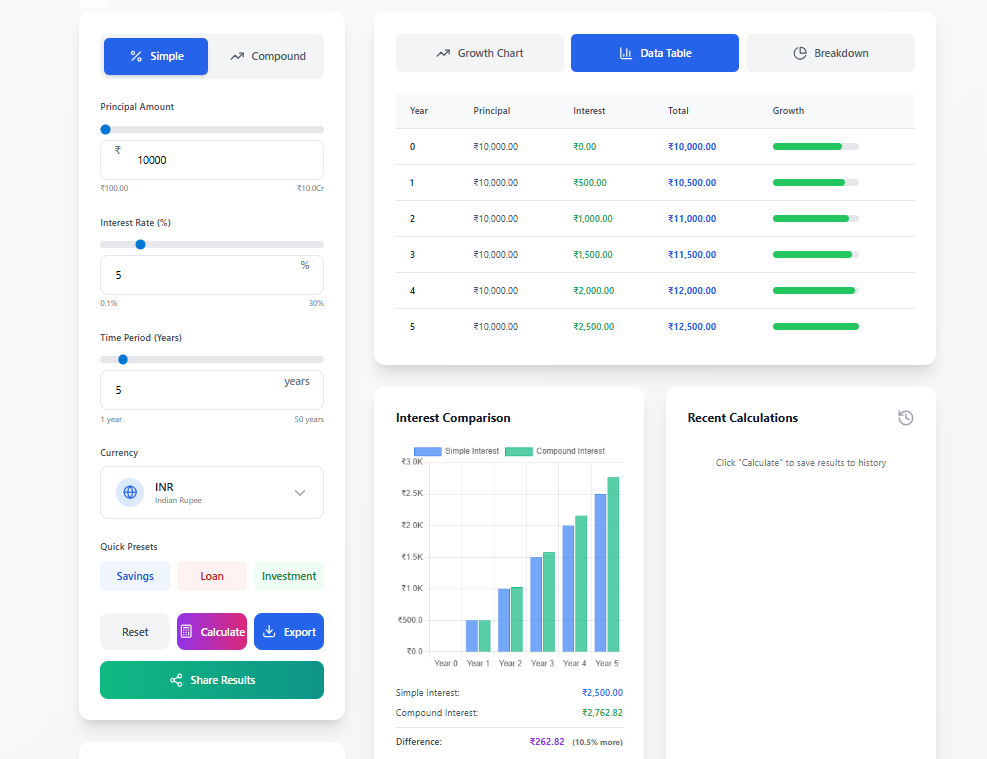

How to Use Our Interest Calculator

Our interest calculator handles both simple and compound interest calculations.

Step 1: Select interest type (Simple or Compound)

Step 2: Enter your numbers:

- Principal amount (how much you borrow or invest)

- Interest rate (annual percentage)

- Time period (in years)

- For compound interest: Choose compounding frequency (annually, quarterly, monthly, daily)

Step 3: Select your currency (over 40 currencies supported)

Step 4: Click Calculate

You will see:

- Total interest earned or owed

- Final total amount

- Year-by-year breakdown

- Growth chart showing your money over time

- Principal vs interest comparison

- Simple vs compound comparison chart

All calculations happen in your browser. Your data never leaves your device.

Real-Life Interest Calculation Examples

Example 1: Credit Card Debt

Scenario: You have $5,000 credit card debt at 18% interest compounded daily. You make no payments for 1 year.

Using the compound interest formula:

- P = $5,000

- r = 0.18

- n = 365

- t = 1

A = 5,000 × (1 + 0.18 ÷ 365) ^ 365 = $5,985

Interest = $985

What this means: Your $5,000 debt grew to nearly $6,000 in just 1 year. This is why credit card debt is so dangerous.

Example 2: Mortgage Loan

Scenario: You take a $300,000 mortgage at 6% interest compounded monthly for 30 years.

Using the monthly payment formula (more complex):

- Monthly payment = about $1,799

- Total paid over 30 years = $1,799 × 360 = $647,640

- Total interest paid = $647,640 - $300,000 = $347,640

What this means: You pay more in interest ($347,640) than the original loan amount ($300,000).

Example 3: Savings for Child's Education

Scenario: You want to save $100,000 for your child's college in 15 years. You can earn 6% compounded monthly. How much do you need to invest today?

Using present value formula:

- A = $100,000

- r = 0.06, n = 12, t = 15

- P = A ÷ (1 + r ÷ n) ^ (n × t)

- P = $100,000 ÷ (1.005) ^ 180 = $40,700

What this means: You need to invest $40,700 today. If you wait 5 years, you would need to invest much more.

Example 4: Retirement Planning

Scenario: You are 30 years old. You want $1,000,000 at age 65. You expect 8% returns compounded annually. How much do you need to invest each month?

Using future value of annuity formula:

- Monthly investment needed = about $500

What this means: Saving $500 per month from age 30 to 65 gives you $1,000,000 at retirement.

Common Interest Calculation Mistakes

Mistake 1: Confusing Simple and Compound Interest

Problem: You think your credit card uses simple interest. It uses compound interest. Your debt grows faster than expected.

Solution: Always check which type of interest applies. Credit cards = compound. Car loans = usually simple.

Mistake 2: Using the Wrong Compounding Frequency

Problem: You calculate compound interest annually, but your savings account compounds daily.

Solution: Check your account terms. Most savings accounts compound daily or monthly.

Mistake 3: Forgetting to Convert Percentage to Decimal

Problem: You use 8 instead of 0.08 in the compound interest formula.

Solution: Remember: 8% = 0.08. Always divide the percentage by 100.

Mistake 4: Ignoring the Effect of Time

Problem: You think starting to save at 35 is fine because you will save more later.

Solution: The example above shows that starting 10 years earlier is worth hundreds of thousands of dollars. Start as early as possible.

Mistake 5: Not Understanding APR vs APY

Problem: Your credit card says 18% APR, but you think that is the annual interest rate.

Solution: APR is the nominal rate. APY (Annual Percentage Yield) includes compounding. For credit cards, the effective rate is higher than the APR.

Interest Rate Reference Table

Here are typical interest rates for different financial products.

| Product | Typical Interest Rate | Compounding | Type |

|---|---|---|---|

| Savings account | 0.5% - 4% | Daily or monthly | Compound |

| High-yield savings | 3% - 5% | Daily or monthly | Compound |

| Certificate of Deposit (CD) | 3% - 5% | Monthly or quarterly | Compound |

| Government bonds | 3% - 5% | Semi-annually | Compound |

| Fixed deposit (India) | 6% - 8% | Quarterly | Compound |

| Car loan | 5% - 10% | Monthly | Simple (usually) |

| Personal loan | 8% - 15% | Monthly | Simple or compound |

| Mortgage | 5% - 7% | Monthly | Compound |

| Student loan | 4% - 8% | Daily or monthly | Simple (federal) |

| Credit card | 15% - 25% | Daily | Compound |

| Stock market (average) | 7% - 10% | Continuous | Compound |

Frequently Asked Questions

Q: How to calculate simple interest on a loan?

A: Use the formula SI = (P × R × T) ÷ 100. For example, $10,000 at 5% for 3 years = (10,000 × 5 × 3) ÷ 100 = $1,500 interest.

Q: How to calculate compound interest on an investment?

A: Use the formula A = P × (1 + r ÷ n) ^ (n × t). Or use our interest calculator for instant results.

Q: What is the difference between simple and compound interest?

A: Simple interest is calculated only on the original principal. Compound interest is calculated on the principal PLUS accumulated interest. Compound interest grows much faster.

Q: What is compounding frequency?

A: Compounding frequency is how often interest is calculated and added to your balance. Options include annually, quarterly, monthly, and daily. More frequent compounding gives higher returns.

Q: How does compounding frequency affect my returns?

A: More frequent compounding gives slightly higher returns. Daily compounding gives more than monthly, which gives more than annual compounding.

Q: What is the best interest calculator online?

A: Our interest calculator is free, supports both simple and compound interest, multiple compounding frequencies, and over 40 currencies.

Q: How to calculate monthly compound interest?

A: Use the formula with n = 12. A = P × (1 + r ÷ 12) ^ (12 × t). Or select "Monthly" in our calculator.

Q: What is the formula for simple interest?

A: Simple Interest = (Principal × Rate × Time) ÷ 100. Total Amount = Principal + Simple Interest.

Q: What is the formula for compound interest?

A: A = P × (1 + r ÷ n) ^ (n × t). Compound Interest = A - P.

Q: How to calculate interest on a savings account?

A: Most savings accounts use compound interest. Use the compound interest formula with daily or monthly compounding. Our calculator does this automatically.

Q: How to calculate interest on a loan?

A: Check if your loan uses simple or compound interest. Car loans are usually simple. Mortgages are usually compound.

Q: What is APR vs APY?

A: APR is the nominal annual rate without compounding. APY includes compounding and shows the actual yearly return. APY is usually higher than APR.

Q: How does time affect compound interest?

A: Time is the most powerful factor in compound interest. The longer your money stays invested, the more it grows due to exponential growth.

Q: Can I calculate interest on a loan with monthly payments?

A: Yes. For simple interest loans, divide the total interest by the number of months. For compound interest, use the loan amortization formula.

Q: Is the interest calculator free?

A: Yes. Completely free. No signup. No limits. Use it as much as you want.

My Final Advice (From 15+ Years of Financial Experience)

After dealing with loans, savings, and investments for over 15 years, here is what I have learned about interest.

Understand what type of interest you are dealing with. Credit cards use compound interest. Car loans use simple interest. Mortgages use compound interest. Knowing the difference helps you make better decisions.

Pay off compound interest debt first. Credit card debt grows exponentially. Pay it off before simple interest debt like car loans.

Start saving early. The examples above show that starting 10 years earlier can be worth hundreds of thousands of dollars. Time is your biggest advantage.

Use compounding to your advantage. For savings and investments, compound interest is your friend. The longer you stay invested, the more your money grows.

Check compounding frequency. For savings accounts, daily compounding is better than monthly. For loans, less frequent compounding is better for you.

Do not just look at the interest rate. For loans, a lower rate with daily compounding might cost more than a slightly higher rate with monthly compounding.

Use a calculator before making financial decisions. Do not guess. Run the numbers. Our interest calculator shows you exactly what you will pay or earn.

And finally, be patient. Compound interest works slowly at first, but after 10-15 years, the growth becomes dramatic. Stick with it.

Calculate Interest Now – Free Tool

Have questions about interest calculation for your specific situation? Leave a comment below. I try to answer every one.

Tags: interest calculator, how to calculate simple interest, simple interest formula, how to calculate compound interest, compound interest formula, simple interest vs compound interest, compound interest frequency, daily compound interest, monthly compound interest, quarterly compound interest, annually compound interest, loan interest calculator, savings interest calculator, investment interest calculator, interest calculation examples, simple interest loan calculator, compound interest investment calculator, interest rate calculator, principal and interest calculator, interest earned calculator, total amount with interest, interest calculation for beginners, compounding frequency explained, power of compounding, interest calculation for 1 year, interest calculation for 5 years, interest calculation for 10 years, interest calculation for 20 years, interest calculation for 30 years, best interest calculator online free, interest calculator with monthly contributions, interest calculator for retirement planning, interest calculator for education planning