How to Start SIP – Complete Guide to Systematic Investment Plan for Beginners

Have you ever wondered how some people build crores of rupees in wealth while earning a normal salary? Or maybe you have heard about mutual funds but do not know where to start?

I remember my first job after college. I was earning ₹35,000 per month. My father kept telling me to start investing. But every time I looked at mutual funds, I felt overwhelmed. There were so many options. Large cap, mid cap, small cap, debt, hybrid. I had no idea what any of it meant.

One day, a colleague told me about SIP. He explained that I could start with just ₹500 per month. That seemed affordable. I started my first SIP of ₹2,000 per month in a large cap fund. That was 8 years ago. Today, that small monthly investment has grown to over ₹3.5 lakhs. I did not have to do anything. I just set it up and forgot about it.

This guide will teach you everything I learned about SIP. No complicated jargon. Just practical advice that helped me start my investment journey.

Quick access: Use our free SIP calculator here

What is SIP? Simple Answer

SIP stands for Systematic Investment Plan. It is a way to invest in mutual funds by putting a fixed amount of money every month, just like a recurring deposit.

Think of it like a monthly bill you pay to yourself. Every month on a fixed date, the money is automatically taken from your bank account and invested in a mutual fund. Over time, these small monthly investments grow into a large corpus.

Simple example:

- Monthly SIP: ₹5,000

- Duration: 20 years

- Expected return: 12% per year

- Total invested: ₹12,00,000

- Final value: Approximately ₹49,95,000

You invest ₹12 lakhs, you get nearly ₹50 lakhs. The extra ₹38 lakhs is the power of compounding working for you.

Why SIP is the Best Investment for Beginners

When I started investing, I had three problems. SIP solved all of them.

Problem 1: I Did Not Have a Large Amount to Invest

I could not afford to invest ₹1 lakh at once. But I could afford ₹2,000 per month. SIP lets you start with as little as ₹500 per month. Anyone with a job can start.

Problem 2: I Did Not Know When to Invest

Should I invest when the market is high or low? I had no idea. SIP removes this problem. You invest the same amount every month. When the market is low, you buy more units. When the market is high, you buy fewer units. Over time, your average cost evens out.

Problem 3: I Kept Forgetting to Invest

I would plan to invest but then forget. SIP is automatic. You set it up once. The money is automatically deducted from your bank account every month. You do not have to remember or do anything.

How SIP Works – The Simple Explanation

Let me explain how SIP works with a simple example.

You decide to invest ₹5,000 every month in a mutual fund. The mutual fund has a Net Asset Value (NAV) which is basically the price of one unit of the fund. NAV changes every day based on the market.

Month 1: NAV is ₹100

- Your ₹5,000 buys 50 units (5000 ÷ 100 = 50)

Month 2: Market goes down. NAV is ₹80

- Your ₹5,000 buys 62.5 units (5000 ÷ 80 = 62.5)

Month 3: Market goes up. NAV is ₹120

- Your ₹5,000 buys 41.6 units (5000 ÷ 120 = 41.6)

After 3 months:

- Total invested: ₹15,000

- Total units: 50 + 62.5 + 41.6 = 154.1 units

- Average cost per unit: ₹15,000 ÷ 154.1 = ₹97.34

Even though the NAV went up and down, your average cost (₹97.34) is lower than the average NAV (₹100). This is called rupee cost averaging. It is the magic of SIP.

The Power of Compounding in SIP

Compounding is when your returns start earning their own returns. It is like a snowball rolling down a hill. It starts small but gets bigger and bigger.

Simple Example of Compounding

Without compounding (simple interest):

- Invest ₹1,00,000 at 10% for 20 years

- Every year you get ₹10,000

- Total after 20 years = ₹1,00,000 + ₹2,00,000 = ₹3,00,000

With compounding:

- Invest ₹1,00,000 at 10% for 20 years

- Year 1 interest = ₹10,000 (total ₹1,10,000)

- Year 2 interest on ₹1,10,000 = ₹11,000 (total ₹1,21,000)

- After 20 years = ₹6,72,000

The difference is huge. Compounding gave you ₹3,72,000 extra.

SIP Compounding Table

Here is how different monthly SIP amounts grow over time at 12% returns.

| Monthly SIP | 10 Years | 15 Years | 20 Years | 25 Years | 30 Years |

|---|---|---|---|---|---|

| ₹1,000 | ₹2.3L | ₹5.0L | ₹9.9L | ₹18.7L | ₹35.2L |

| ₹2,000 | ₹4.6L | ₹10.0L | ₹19.8L | ₹37.4L | ₹70.4L |

| ₹5,000 | ₹11.5L | ₹25.0L | ₹49.5L | ₹93.5L | ₹1.76Cr |

| ₹10,000 | ₹23.0L | ₹50.0L | ₹99.0L | ₹1.87Cr | ₹3.52Cr |

| ₹15,000 | ₹34.5L | ₹75.0L | ₹1.48Cr | ₹2.80Cr | ₹5.28Cr |

| ₹20,000 | ₹46.0L | ₹1.00Cr | ₹1.98Cr | ₹3.74Cr | ₹7.04Cr |

Key insight: The longer you stay invested, the more powerful compounding becomes. The growth from year 20 to year 30 is much larger than from year 0 to year 10.

Types of Mutual Funds for SIP

When I started, I was confused by all the fund types. Here is a simple breakdown.

Equity Funds (High Risk, High Return)

These funds invest mostly in company shares (stocks). They can give high returns but also have high risk.

Large Cap Funds:

- Invest in India's largest 100 companies

- Examples: Reliance, TCS, HDFC Bank

- Risk: Moderate

- Expected returns: 10-12%

- Good for: Long-term goals (7+ years)

Mid Cap Funds:

- Invest in companies ranked 101-250

- Higher growth potential than large cap

- Risk: High

- Expected returns: 12-15%

- Good for: Long-term with higher risk appetite

Small Cap Funds:

- Invest in companies ranked 251 and below

- Very high growth potential

- Risk: Very high

- Expected returns: 15-18%

- Good for: Very long-term (10+ years) with high risk tolerance

ELSS Funds (Tax Saving):

- Same as equity funds but with tax benefits

- 3 year lock-in period

- Tax deduction up to ₹1.5 lakh under Section 80C

Debt Funds (Low Risk, Stable Returns)

These funds invest in bonds, government securities, and other fixed-income instruments.

Risk: Low Expected returns: 6-8% Good for: Short-term goals (1-3 years) and capital preservation

Hybrid Funds (Moderate Risk)

These funds invest in both equity and debt. They balance growth and safety.

Risk: Moderate Expected returns: 9-11% Good for: Medium-term goals (3-7 years)

How to Choose the Right SIP for Your Goals

Based on my experience, here is how to match SIP with your goals.

Goal 1: Retirement Planning

Time horizon: 20-30 years Recommended funds: Equity (large cap + mid cap) Risk tolerance: High (you have time to recover from market falls)

Sample allocation for retirement:

- Large cap: 50%

- Mid cap: 30%

- Small cap: 20%

Monthly SIP needed for retirement:

| Current Age | Monthly SIP (12% returns) | Corpus at 60 |

|---|---|---|

| 25 | ₹5,000 | ₹3.52 Cr |

| 30 | ₹8,000 | ₹3.28 Cr |

| 35 | ₹12,000 | ₹2.96 Cr |

| 40 | ₹20,000 | ₹2.78 Cr |

The earlier you start, the less you need to invest monthly.

Goal 2: Child Education

Time horizon: 15-18 years Recommended funds: Equity (large cap + mid cap) Risk tolerance: Moderate to high

Sample allocation for child education:

- Large cap: 60%

- Mid cap: 30%

- Debt: 10% (for safety as goal approaches)

Monthly SIP needed for ₹50 lakhs college fund:

| Child's Age | Monthly SIP (12% returns) |

|---|---|

| 1 year | ₹3,500 |

| 5 years | ₹7,500 |

| 10 years | ₹18,000 |

| 13 years | ₹35,000 |

Goal 3: Home Down Payment

Time horizon: 5-10 years Recommended funds: Hybrid (equity + debt) Risk tolerance: Moderate

Sample allocation for home down payment:

- Equity: 50%

- Debt: 50%

Goal 4: Vacation or Wedding

Time horizon: 2-5 years Recommended funds: Debt or hybrid Risk tolerance: Low

Sample allocation for short-term goals:

- Debt funds: 70%

- Equity: 30%

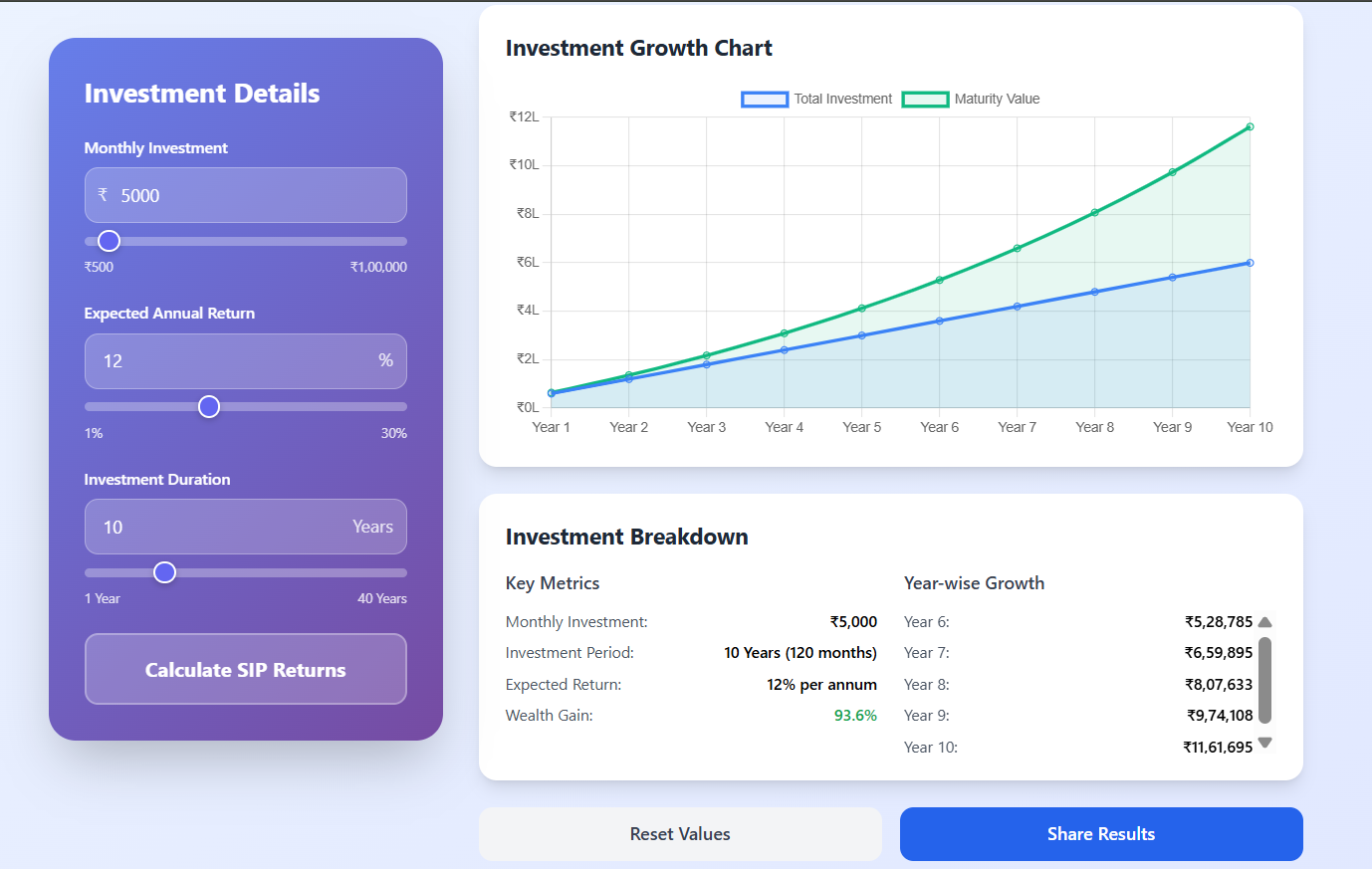

How to Use a SIP Calculator

Our SIP calculator helps you plan your investments. Here is how to use it.

Step 1: Enter Your Monthly Investment

Enter how much you can invest every month. Start with any amount. Even ₹500 is fine.

Step 2: Select Investment Duration

Choose how many years you want to invest. Longer duration gives higher returns due to compounding.

Step 3: Enter Expected Return Rate

- Conservative: 8-10% (debt funds)

- Moderate: 10-12% (hybrid funds)

- Aggressive: 12-15% (equity funds)

Step 4: View Results

The calculator shows:

- Total amount you invested

- Estimated returns (profit)

- Final maturity value

- Year-by-year growth

Real Example Using SIP Calculator

Scenario: You want to know how much to invest monthly to get ₹1 crore in 20 years at 12% returns.

Using the calculator:

- Target amount: ₹1,00,00,000

- Duration: 20 years

- Return rate: 12%

- Calculator shows: ₹13,500 monthly

Answer: Invest ₹13,500 per month for 20 years to reach ₹1 crore.

Step-Up SIP (Top-Up SIP) – Increase Investments Over Time

As your income grows, you should increase your SIP amount. This is called step-up SIP or top-up SIP.

Why Step-Up SIP Matters

If you start with ₹5,000 monthly at age 25 and never increase, you will have ₹3.52 crore at age 60.

But if you increase your SIP by 10% every year:

- Year 1: ₹5,000 monthly

- Year 5: ₹7,300 monthly

- Year 10: ₹11,800 monthly

- Year 20: ₹30,600 monthly

Result at age 60: ₹8.2 crore (instead of ₹3.52 crore)

How to Implement Step-Up SIP

Method 1: Automatic (if fund allows) Some mutual funds offer automatic step-up. You set the percentage increase once. It happens automatically every year.

Method 2: Manual (do it yourself) Every year on your birthday or appraisal month, increase your SIP by 10-15%.

Method 3: Income-linked Whenever you get a salary hike, increase your SIP by half the hike amount.

SIP vs Other Investment Options

SIP vs Recurring Deposit (RD)

| Feature | SIP | RD |

|---|---|---|

| Returns | 10-15% (market linked) | 5-7% (fixed) |

| Risk | Medium to High | Very Low |

| Tax on returns | LTCG 10% after ₹1L | As per income slab |

| Best for | Long-term (5+ years) | Short-term (1-3 years) |

My advice: Use RD for emergency funds and short-term goals. Use SIP for long-term wealth creation.

SIP vs PPF

| Feature | SIP | PPF |

|---|---|---|

| Returns | 10-15% | ~7% (government fixed) |

| Lock-in | None (can withdraw anytime) | 15 years |

| Tax benefit | ELSS only (3 year lock-in) | Section 80C |

| Best for | Growth | Safety + tax saving |

My advice: Use PPF for your debt allocation and tax saving. Use SIP for equity allocation and growth.

SIP vs Lump Sum

| Feature | SIP | Lump Sum |

|---|---|---|

| Timing risk | Spread out | Concentrated |

| Capital needed | Small monthly | Large one-time |

| Discipline | Built-in | Requires self-control |

| Best for | Regular income, beginners | Windfall gains, experienced investors |

My advice: Most people should start with SIP. Once you have a large corpus, you can consider lump sum.

ELSS SIP for Tax Saving

ELSS (Equity Linked Savings Scheme) is an equity fund that gives tax benefits under Section 80C.

ELSS Key Features

- Tax deduction: Up to ₹1.5 lakh per year

- Lock-in period: 3 years (shortest among 80C options)

- Returns: 12-15% historically

- Risk: High (like other equity funds)

How to Use ELSS SIP for Tax Saving

To claim full ₹1.5 lakh deduction under Section 80C:

- Monthly ELSS SIP = ₹1,50,000 ÷ 12 = ₹12,500

Example:

- You invest ₹12,500 monthly in ELSS

- Total yearly investment = ₹1,50,000

- Tax saved (30% slab) = ₹45,000

- Your effective investment after tax saving = ₹1,05,000

ELSS Lock-in Rules

Each monthly SIP has its own 3-year lock-in.

Example:

- January 2025 SIP → can withdraw January 2028

- February 2025 SIP → can withdraw February 2028

- March 2025 SIP → can withdraw March 2028

Common SIP Mistakes to Avoid

Mistake 1: Stopping SIP During Market Crash

When the market falls, people panic and stop their SIP. This is exactly when you should continue or even increase.

Why: When the market is down, you buy more units for the same amount. When the market recovers, those extra units give higher returns.

What I learned: My best returns came from the SIPs I continued during the 2008 crash and 2020 COVID crash.

Mistake 2: Choosing Funds Based Only on Past Returns

Last year's best performer may not be next year's best performer.

What to do instead:

- Look at 5-10 year track record

- Check fund manager experience

- Compare expense ratio

- Ensure consistency, not just one good year

Mistake 3: Having Too Many SIPs

Some people have 20-30 different SIPs. This is hard to track and manage.

What to do:

- 4-6 SIPs are enough

- One large cap

- One mid cap

- One small cap (if high risk tolerance)

- One ELSS (for tax saving)

- One debt or hybrid (for balance)

Mistake 4: Ignoring Expense Ratio

Expense ratio is the fee the mutual fund charges. Higher fees mean lower returns.

Example on ₹10 lakhs over 20 years:

- Expense ratio 1% → you pay ₹2.2 lakhs in fees

- Expense ratio 0.5% → you pay ₹1.1 lakhs in fees

What to do: Choose direct plans instead of regular plans. Direct plans have lower expense ratios.

Mistake 5: Not Increasing SIP Over Time

Your income grows, but your SIP stays the same. You are missing out.

What to do: Increase your SIP by 10% every year or whenever you get a salary hike.

How to Start Your First SIP – Step by Step

Here is exactly how I started my first SIP. Follow these steps.

Step 1: Complete KYC

You need to complete KYC (Know Your Customer) before investing. This is a one-time process.

Documents needed:

- PAN card

- Aadhaar card

- Bank statement or cancelled cheque

- Passport size photo

How to do KYC:

- Online through any fund house website

- Through apps like Groww, Zerodha, Paytm Money

- At any bank branch

Step 2: Choose a Fund

For your first SIP, keep it simple. Choose a large cap fund or an index fund.

Good first SIP options:

- UTI Nifty Index Fund

- SBI Bluechip Fund

- HDFC Index Fund

Step 3: Decide Monthly Amount

Start with an amount that does not feel like a burden. Even ₹500 is fine.

Rule of thumb: Save at least 20% of your income. Half of that can go into SIP.

Example for ₹50,000 monthly salary:

- 20% savings = ₹10,000

- SIP = ₹5,000 to ₹7,000

- Remainder in emergency fund or RD

Step 4: Set Up Auto-Debit

Choose a date for your SIP. I recommend the 3rd or 5th of every month. This gives time for salary credit.

Setup process:

- Log in to the fund house or investment app

- Select the fund

- Enter monthly amount

- Select date

- Provide bank account details

- Authorize auto-debit mandate

Step 5: Track and Review

Set a reminder to review your SIP once a year.

What to check:

- Is the fund performing as expected?

- Can you increase the amount?

- Are your goals on track?

Real-Life SIP Examples

Example 1: The Early Starter (Age 25)

Profile: Ramesh, 25 years old, monthly salary ₹40,000 Goal: Retirement corpus of ₹5 crore at age 60 SIP plan:

- Start SIP: ₹6,000 monthly

- Increase: 10% every year

- Fund type: Equity (large cap + mid cap)

Using SIP calculator:

- Year 1: ₹6,000 monthly

- Year 10: ₹14,000 monthly

- Year 20: ₹36,000 monthly

- Year 30: ₹95,000 monthly

Result at age 60: ₹5.2 crore

Example 2: The Mid-Career Starter (Age 35)

Profile: Priya, 35 years old, monthly salary ₹1,20,000 Goal: ₹3 crore for retirement at age 60 SIP plan:

- Start SIP: ₹25,000 monthly

- Increase: 10% every year

- Fund type: Equity + hybrid

Result at age 60: ₹3.1 crore

Example 3: Child Education Goal

Profile: Rajesh, 40 years old, daughter age 8 Goal: ₹50 lakhs for college when daughter turns 18 (10 years) SIP plan:

- Monthly SIP: ₹22,000

- Fund type: Hybrid (60% equity, 40% debt)

- Expected return: 11%

Result: ₹50.2 lakhs after 10 years

SIP Returns – Historical Performance

Here is how different types of SIPs have performed historically.

| Fund Type | 5 Year Returns | 10 Year Returns | 15 Year Returns |

|---|---|---|---|

| Large Cap | 11-13% | 12-14% | 13-15% |

| Mid Cap | 13-16% | 14-17% | 15-18% |

| Small Cap | 15-20% | 16-19% | 16-20% |

| ELSS | 12-15% | 13-16% | 14-17% |

| Hybrid | 9-11% | 10-12% | 11-13% |

| Debt | 6-8% | 7-8% | 7-8% |

Note: Past performance does not guarantee future returns. These are only for reference.

Frequently Asked Questions

Q: How to start SIP for beginners?

A: Complete KYC, choose a fund (start with large cap), decide monthly amount (as low as ₹500), set up auto-debit. Use our SIP calculator to plan.

Q: What is the minimum amount for SIP?

A: Most mutual funds allow SIP starting from ₹500. Some funds have ₹1,000 minimum.

Q: How to calculate SIP returns?

A: Use our SIP calculator. Enter monthly amount, duration, and expected return rate.

Q: Is SIP safe?

A: SIP in equity funds has market risk. But over long periods (7+ years), equity has historically given good returns. For safety, choose debt funds.

Q: Can I withdraw SIP anytime?

A: Yes, except ELSS funds which have 3-year lock-in. For other funds, you can withdraw anytime.

Q: What is the best SIP for 10 years?

A: For 10 years, large cap or mid cap equity funds are good. Use our SIP calculator to see potential returns.

Q: How much to invest in SIP monthly?

A: Save at least 20% of your income. Half of that can go into SIP. Use our calculator to see what you need for your goals.

Q: What is step-up SIP?

A: Step-up SIP means increasing your monthly investment amount every year. This helps you invest more as your income grows.

Q: Is SIP good for retirement?

A: Yes. SIP in equity funds is one of the best ways to build retirement corpus due to long-term compounding.

Q: What is the difference between SIP and mutual fund?

A: SIP is a method of investing in mutual funds. You can also invest lump sum in mutual funds.

Q: How to choose SIP fund?

A: Look for funds with consistent 5-10 year performance, low expense ratio, and experienced fund manager.

Q: Is SIP taxable?

A: Yes. For equity funds, LTCG (holding >1 year) above ₹1 lakh is taxed at 10%. For debt funds, gains are taxed as per income slab.

Q: Can I have multiple SIPs?

A: Yes. You can have different SIPs for different goals. But keep it simple. 4-6 SIPs are enough.

Q: What happens if SIP auto-debit fails?

A: Most funds give a grace period of 30 days. If you pay within that, the SIP continues. After multiple failures, the SIP may be stopped.

Q: Is SIP calculator accurate?

A: SIP calculators give estimates based on assumed returns. Actual returns depend on market performance.

My Final Advice

After investing through SIPs for 8 years, here is what I have learned.

Start today, not tomorrow. The best time to start SIP was 10 years ago. The second best time is today. Do not wait for the perfect time.

Start small, but start. Even ₹500 per month is fine. What matters is starting the habit. You can always increase later.

Do not stop during market falls. This is when SIP works best. You buy more units at lower prices. When the market recovers, those extra units give higher returns.

Increase your SIP regularly. Every year, increase your SIP by 10% or whenever you get a salary hike. This makes a huge difference over time.

Keep it simple. You do not need 20 different funds. 4-6 good funds are enough. Large cap, mid cap, ELSS, and one debt fund.

Think long-term. SIP is not for getting rich in 1-2 years. It is for building wealth over 10-20-30 years. Be patient.

And finally, use a good SIP calculator. It helps you set realistic goals and see what you need to invest.

Calculate Your SIP Returns Now – Free Tool

Have questions about starting your SIP journey? Leave a comment below. I try to answer every one.

Tags: sip calculator, how to start sip, systematic investment plan, mutual fund sip, sip investment guide, sip calculator online, sip return calculator, sip monthly investment calculator, what is sip, sip benefits explained, power of compounding in sip, rupee cost averaging in sip, sip vs lump sum, sip vs rd, sip vs ppf, how much to invest in sip, sip for beginners, sip for retirement, sip for child education, sip for home purchase, step up sip, top up sip, elss sip for tax saving, sip calculator with step up, sip calculator for 10 years, sip calculator for 15 years, sip calculator for 20 years, sip calculator for 30 years, sip investment strategies, how to choose sip funds, sip mistakes to avoid, sip portfolio allocation by age, sip goal planning, sip monthly calculator, best sip plans, sip returns historical, sip tax benefits, sip withdrawal rules, sip vs mutual fund lump sum, sip investment for salaried employees